The situation involving Blue Owl Capital has progressed beyond basic liquidity management. It now serves as a primary case study of the consequences that arise when internal valuation models, redemption commitments, and market realities intersect.

In recent weeks, the situation has shifted from temporary stress to a fundamental structural change. A convergence of red flags has emerged, including redemption gates, a terminated merger, third-party tender offers at significant discounts, and partial capital distributions. Collectively, these developments indicate that the issue has evolved from a liquidity event to a credibility event.

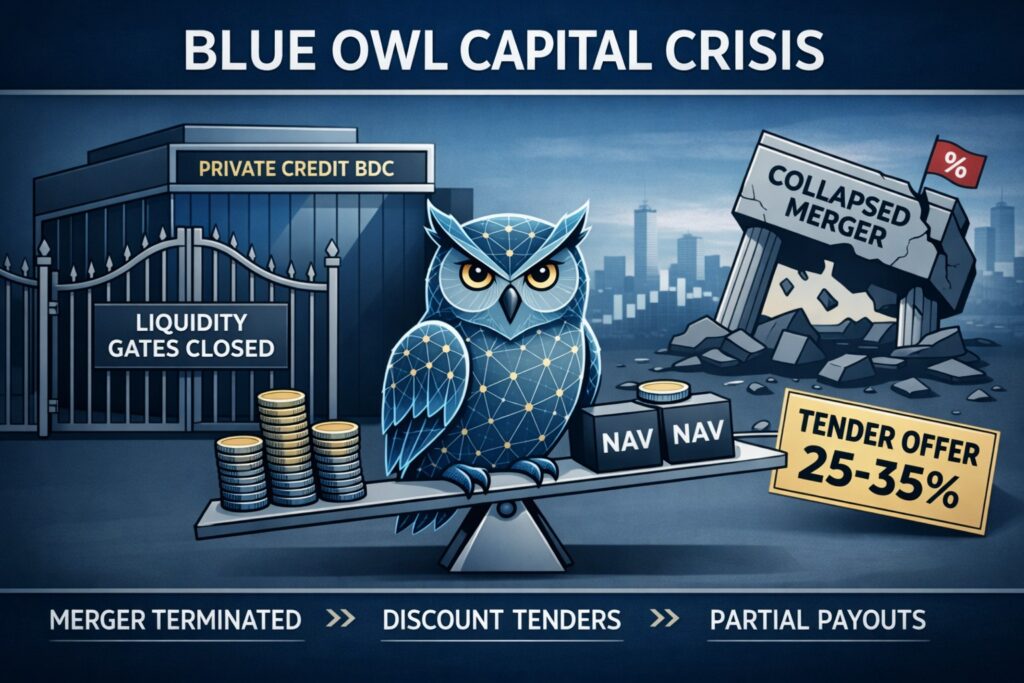

The Merger That Didn’t Happen

A significant development is the formal termination of the planned merger between the publicly traded OBDC and the non-traded OBDC II. Although initially presented as a strategic consolidation intended to “enhance shareholder value,” the transaction failed due to investor resistance and market discount pressures.

Shareholder opposition to a merger, prompted by shares trading significantly below the stated Net Asset Value (NAV), signals that the market does not accept the company’s valuation. This has legal implications. If a transaction is promoted as “stabilizing” while material valuation uncertainties are known but not fully disclosed, it may expose the company to substantial investor claims.

Discount Tender Offers: The Market Sets the “Shadow Price”

A notable development is the emergence of third-party tender offers. Firms such as Saba Capital and Cox Capital have reportedly provided liquidity to investors, but at significant discounts. These firms are offering to purchase shares at prices 20% to 35% below the stated NAV.

These offers represent calculated investment strategies rather than benevolent actions. When sophisticated external investors are only willing to purchase shares at a 30% discount, this effectively establishes a “shadow price” for the fund. For retail investors who acquired these BDCs as stable income vehicles, a 25% or 30% discount reflects a structural repricing of their retirement savings, rather than ordinary market volatility.

The 30% Return-of-Capital: A Partial Exit

Blue Owl’s reported plan to distribute approximately 30% of NAV through asset sales does not constitute a traditional redemption. Instead, it represents a partial realization event. Investors are not permitted to exit at full value; they receive a portion of their capital while the remainder remains invested in an illiquid loan portfolio.

This situation highlights two significant realities:

- The manager is attempting to alleviate redemption pressure without initiating a complete liquidation.

- Asset sales may be occurring at levels that indicate the internal valuation models have overstated the value of the loans.

The Software Exposure: An AI-Driven Risk

Blue Owl is heavily concentrated in software and technology borrowers. As Generative AI accelerates structural change in legacy software business models, the risk profile of these loans has shifted overnight. If the underlying companies are struggling to compete in an AI-driven world, the loans backing them are worth less.

Broker Due Diligence and the “Bond Substitute” Trap

A significant percentage of Blue Owl’s BDC exposure was sold through brokerage channels to retirees. Under FINRA rules, brokers have a strict “Regulation Best Interest” (Reg BI) obligation. They must:

- Conduct deep due diligence on complex products, such as BDCs.

- Ensure the investment is suitable for a client’s specific liquidity needs.

- Avoid presenting illiquid, high-risk credit vehicles as “bond substitutes.”

If an advisor emphasized “quarterly liquidity” and “stable income” without explaining that the exit door could be locked at any time, that advisor—and their firm—may be liable for the resulting losses.

The Legal Frontier: Accountability in the New Market

When liquidity gates close and third-party buyers demand 30% discounts, investor confidence shifts from performance to accountability. The next phase of the Blue Owl story will likely unfold in FINRA arbitration and shareholder litigation venues rather than on the trading floor.

Sonn Law Group, led by Jeffrey Sonn, holds Wall Street accountable for exactly these types of “liquidity illusions.” Jeff’s expertise in navigating the intersection of complex financial products and broker misconduct is recognized industry-wide.

What Investors Should Consider Now

If you hold shares in a Blue Owl BDC or any non-traded private credit vehicle, you should immediately review:

- The original marketing materials and the “assurances” given about NAV stability.

- Any written or verbal claims by your broker that the fund offered “easy exits.”

- The actual fulfillment rate of your recent redemption requests.

The difference between “limited liquidity” and “effectively locked capital” is legally meaningful. If you believe the risks of this investment were understated, a consultation with experienced securities counsel is your next step.

CONTACT US FOR A FREE CONSULTATION

Se Habla Español

Contact our office today to discuss your case. You can reach us by phone at 844-689-5754 or via e-mail. To send us an e-mail, simply complete and submit the online form below.